LEE COUNTY, Fla. — Two months after Hurricane Ian hit Southwest Florida, we’re finding out that homeowners with damage are struggling with insurance claim payouts.

“You pay your insurance and you expect to get that back, especially when you've never had a claim in almost 30 years we've lived in that home,” exclaimed Iona Homeowner Teresa Hall. “I'm flabbergasted. Really, I just think it's so upsetting. I mean, it makes it hard to sleep at night. What are we ever going to get back in our home? Can we afford to get back in our home?”

Teresa and her husband, Matt Hall, live in the Iona neighborhood of Fort Myers and work for nonprofits on Captiva and Sanibel Island-- all hit by Hurricane Ian at the end of September.

Ian flooded their entire home and damaged their $50,000 dollar solar panel roof, pool enclosure and outside storage.

“We just spent a bunch of money new roof, we've redone the plumbing read, everything was up to code,” Matt Hall explained.

One week after filing their claim, it rained and when he returned to check on the house, Matt said, “I heard a waterfall in our house and we had two bedroom ceilings collapse, insulation, drywall and everything."

At the end of October, their insurance company sent a few checks for about $6,000 dollars that were their payout after their policy’s $18,000 dollar deductible.

“We tried to do our own due diligence, what we're supposed to do because when you drive through Florida, especially Lee County, ‘Don't call a public adjuster, don't…’ you know all these this campaigns of not using a public adjuster,” Matt stressed.

The couple said they were scared to seek help because the state’s Chief Financial Officer (CFO), Jimmy Patronis, was warning hurricane victims to not sign contractors and public adjusters.

For example, on Oct. 18, Patronis posted a video on Facebook stating, “Do not sign anything. There are unscrupulous players out there, in addition to the good ones, but don’t be taken advantage of.”

“We have a lot of ethics and honesty and we want to do the right thing all the time, but when you get just shut down to the point where you're not even getting responses back from your insurer,” Teresa Hall explained that’s when they decided to hire help.

“The insurance company closed these peoples’ claim before they even had a copy of their policy,” said Rick Tutwiler of Tutwiler & Associates Public Adjusters out of Tampa.

Tutwiler told us that he spent a month trying to get the Hall’s claim reopened, hearing back on November 15.

“We are in receipt of your letter of rep…” he read the email to ABC Action News Reporter Stassy Olmos the day it came in.

Tutwiler said the Hall’s are just two of the hundreds of Ian victims he’s trying to help, and he adds that their story isn’t the worst of them.

“A few hundred, yeah, and they range from homeowners to hotels. We try to help everybody,” he said.

We spoke with another public adjuster, Mendy Lipszyc, of Panther Public Adjusting out of Miami, to see if he was inundated as well.

“Last week alone, we signed about 20 to 25 clients,” Lipszyc said in mid-November.

“These are all people whose insurance has come back with claims that are just far below what they believe they deserve?” Olmos asked.

Lipszyc said it’s hurricane victims who feel shorted, as well as those who can’t get ahold of their insurance company.

“Some of the stuff we're seeing is simply outrageous,” Lipszyc added.

He explained that many property insurance companies are denying claims saying they’re the result of flooding and not covered under the standard homeowner's policy.

“I went in after this homeowner was denied. I went on the roof; there is puncture holes in her metal roof... that's not caused by flooding,” Lipszyc exclaimed.

The Florida Association of Insurance Agents warned hiring an adjuster will cost homeowners money because they take 10% of a claim when a state of emergency is declared.

I asked Florida’s state-backed property insurer, Citizens Property Insurance Corps, when a homeowner would be valid in hiring help.

“What we have always said… give your insurance company the chance to do the right thing, and I think that nine chances out of ten, that’s going to take care of your policy,” said Michael Peltier a spokesperson for Citizens.

We then went to the American Policyholder Association (APA) Executive Director Doug Quinn for his advice.

“If somebody feels that they are being cheated by their insurance carrier, they see something that they feel is dishonest or illegal; it never hurts to get a consultation with a professional, such as a public adjuster or an attorney,” Quinn advised.

He adds that the APA has been fielding complaints regarding insurance companies out of Hurricane Ian already. He said some are from homeowners and some are from adjusters hired by the insurance companies.

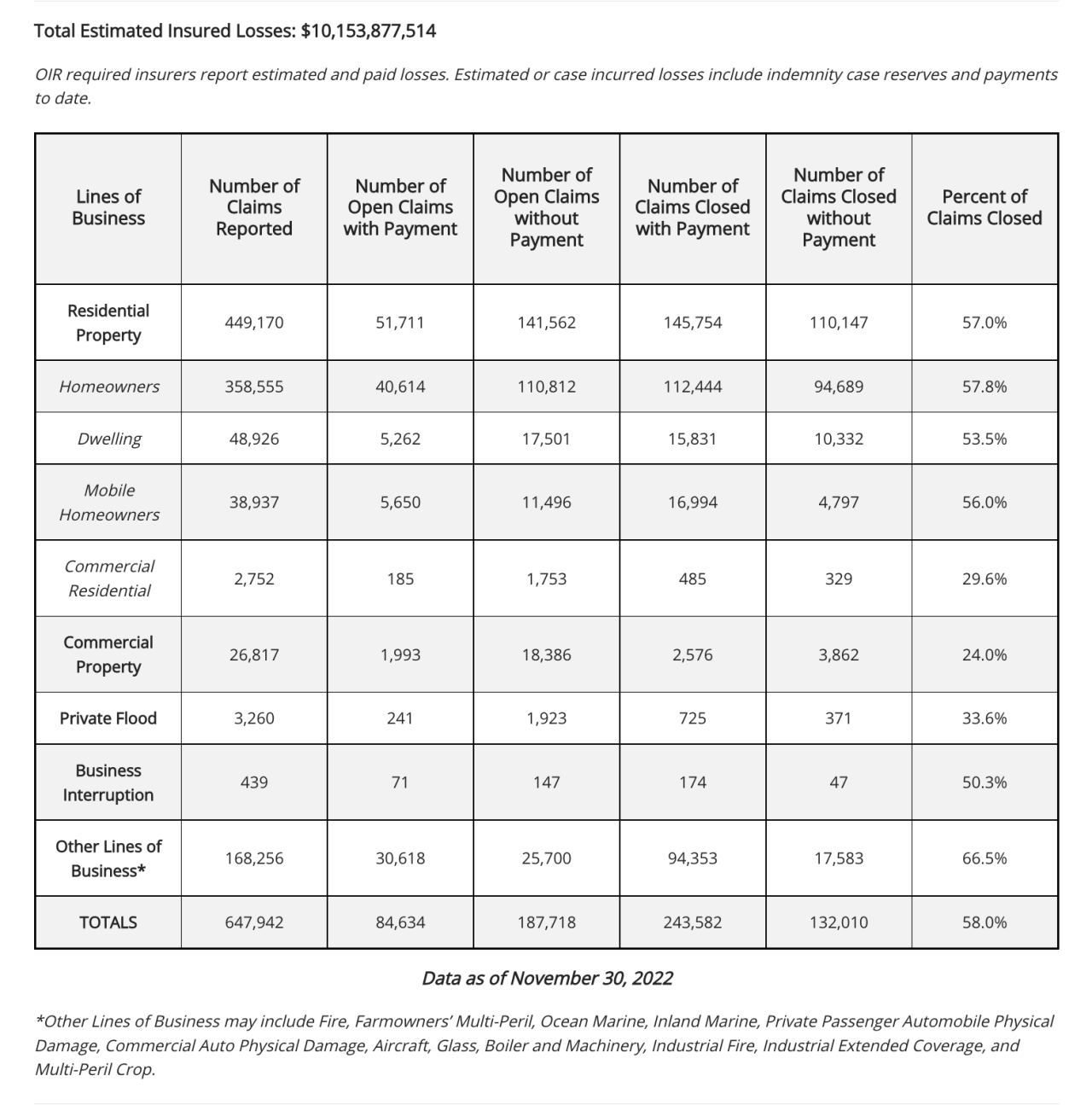

According to the Office of Insurance Regulation (OIR) claims database, more than 358,000 homeowners have filed claims out of Hurricane Ian as of November 30. The department is reporting almost 95,000 claims closed without payment, and more than half of total claims closed in general.

The Halls said that they tried to call and reach out online to the CFO’s office for help with their claim but never heard back.

On November 10th, they wrote a letter to Patronis and still, they said they have not heard back.

“I'm reaching out to Tallahassee… to the boss, right, the one that's out there saying don't pay anything, you paid for your insurance, call your insurance company… and here we are,” Matt Hall said.

On November 18th, we reached out to both the CFO’s office as well as OIR with several questions regarding homeowners’ concerns.

On December 7, a spokesperson for OIR said in an email statement:

“OIR expects insurers to do everything possible to respond to the needs of impacted Floridians, restore a sense of normalcy, and facilitate restoration and recovery in impacted communities. Consumers are encouraged to work closely with their insurance company and agent if they feel they have been wrongfully denied or unfairly compensated regarding a claim. Consumers should first provide the insurer with damage estimates or additional documentation to support their claim.”

Olmos also tried the process of filing a complaint through the CFO and OIR herself.

The contact link on the CFO’s website returned an error page stating “file or directory not found” as soon as she selected the option to “file an insurance complaint.” She was able to get to the submission page through the “Report an Insurance Concern Online” button under “Get Insurance Help.”

When she tried calling the (877) My-FL-CFO number at the end of November, she waited 20 minutes before she was transferred to an overflow line where an employee who claimed to be from another department said she could take the complaint.

When clicking the consumer helpline link on the OIR’s website, it links to the same CFO error page.

Neither office has answered our questions regarding the broken link.

We also reached out to the Hall’s insurance company. A spokesperson said in an email that they received a letter from a public adjuster representing the Halls on November 1. They said it “included new photographs showing interior damage caused by post-Ian rains, as well as additional repair estimates. The claim was reopened on November 15 and will be readjusted.”

“When it's your home and you have no roof, and they're offering you a third of the cost offering a third of the cost. How could you not hire an attorney or an adjuster to represent you?” Matt Hall exclaimed. “I don't want to get emotional,” he paused, “But without them, I don't know where we'd be.”

We spoke with another Ian victim struggling with her insurance claim. The homeowner did not want to be identified, but she owns a manufactured home in Venice and lost her carport and entire front room-- which she said her insurance company wrote as a “weather-tight room,” disqualifying it from coverage.

She had been calling her insurance and fighting back for a month and a half at the time we spoke with her.

When we reached out to her insurance company, we were able to confirm that sometimes insurance adjusters can miss things.

The company told us in an email response:

“The Adjuster originally did not write for the weather-tight room; however, during the desk review process, the mistake was corrected and the weather-tight room was included in the check.”

Even then, the homeowner told us that the check still wasn’t enough for repairs, so she’s now seeking a public adjuster.

Tutwiler added that homeowners should not be discouraged from hiring a "consumer advocate like public adjusters." In reference to the CFO's statements, he said, "I understand, there's good and there's bad out there. We're highly regulated by the Department of Financial Services as it is... so if there are bad actors out there, enforce something on them, suspend their licenses or do something, but don't cast a broad net on all public adjusters."

So what can a homeowner do when they’re worried about receiving a fair claim?

Here are some tips from the American Policyholder Association:

- Take pictures of all damage from all directions

- Document all communication with all carrier employees

- Videotape any inspections to document the actions of an adjuster

- Request copies of your policy and the inspection report

- File any concerns or complaints with your insurance company to the executive suite; this is known as a “Presidential complaint”

- File any complaints with the state’s insurance office, including documentation

Policyholders can find more advice on how to advocate for themselves with their insurance company on the APA website here. For specific advice after natural disasters, visit the APA website here.

One of the biggest concerns for Ian victims right now is waiting for what’s called mediation.

That’s when the CFO’s office sets up a location with a third party to mediate claims between homeowners and insurance companies. Two months after Hurricane Ian and the CFO’s office has not released any information regarding mediation.

One question homeowners may have is if they cash a check sent by their insurance company -- does that mean they are accepting the claim and the funds as final payment?

Tutwiler explains it's not binding unless the check or accompanying letter states that by cashing the check it means final payment.

We have also found that some companies offer discounts when writing policies that give homeowners no option but to either accept payment or the insurance company will send their own contractors to do the work.

We did a report after Hurricane Ian with several insurance experts warning of door-knockers looking to scam hurricane victims -- often contractors who get homeowners to sign what’s called an assignment of benefits or AOB, allowing a third party, often a roofer, to take over with the insurance company.

According to the OIR, the abuse of AOBs has fueled runaway litigation, putting millions of dollars from insurance companies into the pockets of roofers and their attorneys and now driving up the cost of all homeowners’ premiums.

Nationwide, Florida represents about 9% of claims, but 79% of claims lawsuits. Experts say it’s these underwriting costs that have caused more than a dozen carriers to pull out of the state or go bankrupt in the last few years.

These are all concerns that everyone in the insurance industry, from insurance companies to public adjusters, hope will be up included in the Florida legislature’s special session starting Monday, Dec. 12.

It’s the second special session called this year for property insurance reform.

Governor Ron DeSantis's office told us that the session aimed to “pass additional reforms to further stabilize Florida’s property insurance market that will introduce more competition and policies designed to lower the prices for consumers.”

On Tuesday, the house speaker and senate president issued a proclamation for the special session with a list of legislation they aim to tackle.

They are as follows:

- Reduce the cost of litigation regarding property insurance claims.

- Foster the availability of reinsurance for property insurance.

- Improve claims handling practices in property insurance

- Modify deadlines for notices of property insurance losses and limit the assignment of benefits under property insurance policies.

- Prescribe property insurance requirements regarding alternative dispute processes, coverage options, and agent practices.

- Increase oversight of property insurance market participants

- Improve the financial stability of the Citizens Property Insurance Corporation, reduce the potential for assessments related to the Citizens Property Insurance Corporation, and foster the transition of Citizens Property Insurance Corporation policies to the private property insurance market.

- Provide tax relief and other financial assistance related to damages resulting from Hurricanes Ian and Nicole.

- Provide additional mechanisms to support the Division of Emergency Management for natural disaster response, recovery, and relief efforts.

- Establish a statewide toll credit program for frequent Florida commuters.

- Provide appropriations to implement such legislation.

The OIR also advised in their email statement:

“OIR encourages consumers who having issues with a claim to report it; consumers can report issues with claims on DFS’ website here [myfloridacfo.com]. This will assist the State in reviewing applicable information related to the claim and determining what action can be taken to assist the consumer. If needed, there are alternative dispute resolution processes available to policyholders, such as mediation and appraisal. Consumers may request mediation with the DFS Division of Consumer Services or follow the guidance in their policy for requesting appraisal.”