ST. PETERSBURG, Fla. — Thousands of Floridians could soon be paying bigger premiums to protect their homes against flooding.

“I’ve lived on the beaches and in this community since 1983. I raised my girls here you know and I’ve helped people buy and sell homes," said Melinda Pletcher, a City of St. Pete Beach Commissioner and real estate agent for Smith and Associates. "“Today’s a big day when it comes to flood insurance in this area.”

Friday, the National Flood Insurance Program (NFIP) is changing the program that determines the rates for policyholders.

RELATED: What to expect when flood insurance premiums change on Oct. 1

Known as Risk Rating 2.0, the Federal Emergency Management Agency (FEMA) says the new program will create more “equitable” and “informed” rates by considering a property’s cost to rebuild and other factors to generate a “true flood risk.”

The NFIP program was established by Congress in 1968, and according to the Wharton Center for Risk Management and Decision Processes, the “vast majority” of flood insurance policies in Florida are written and insured by the NFIP. According to FEMA, there are 1,727,900 in the state.

Beginning Oct. 1, new policies will be subject to the new program’s rating method, which focuses more emphasis on the value of the structure. All remaining policies renewing on or after Apr. 1, 2022, will be subject to the new rating method.

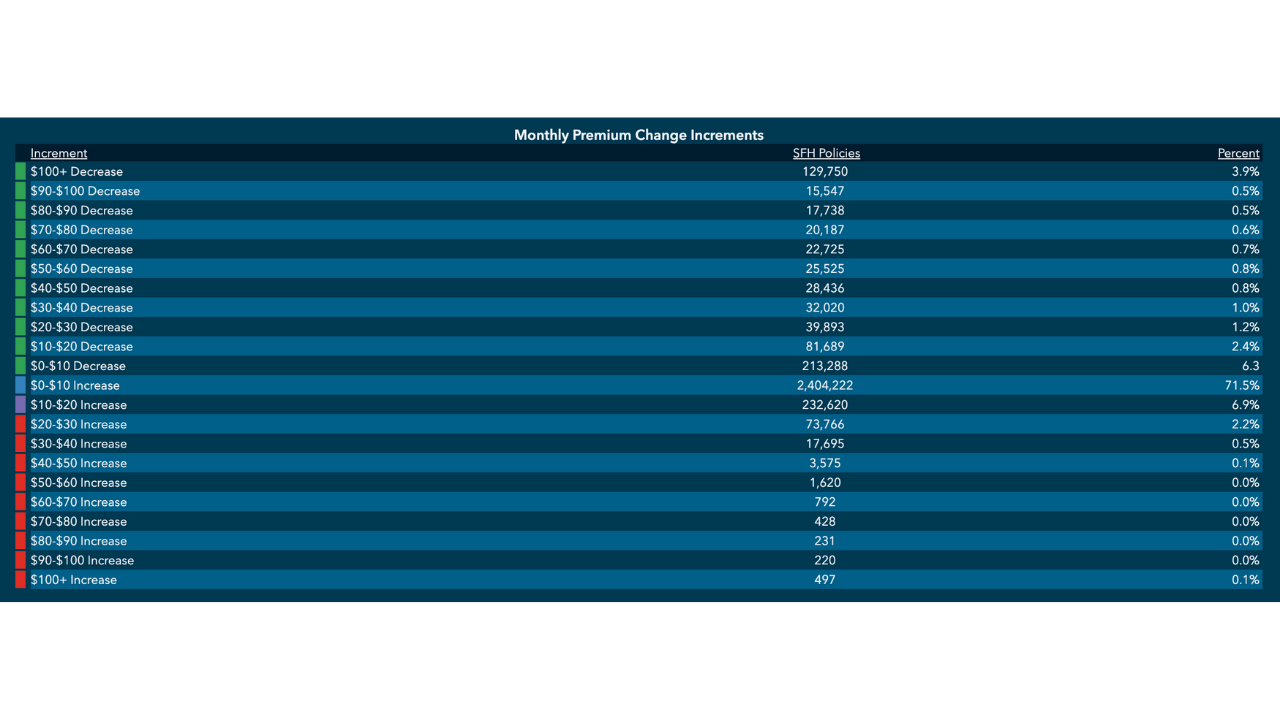

According to FEMA, “96% of current policyholders’ premiums will either decrease or increase by $20 or less per month under Risk Rating 2.0.”

However, Jake Holehouse, an insurance agent and flood insurance advocate in Pinellas County said that’s not the whole story.

He said some homeowners are already seeing “massive” increases on new policies, and he worries some homeowners’ insurance premiums will keep climbing each year, ballooning from hundreds to thousands of dollars annually.

“It’s huge. It’s the biggest change that’s happened to the FEMA flood program since the 1970s,” he said. “From a state level, we’re seeing that 80% of Floridians are going to see higher rates on this new flood insurance program. From a local level, we’re estimating that it’s probably closer to 90 or 95% of policyholders long-term will see increased flood insurance rates as a result of this.”

“A FEMA compliant home that was built to 6 feet above base flood, exceeding all expectations of what FEMA‘s goals and directives were," said Pletcher, will now get the short end of the stick. She says her neighbors will see their yearly $680 policy jump overtime to around $12,000. “It’s almost penalizing people who are doing things exactly how they would want you to do.”

She thinks it’ll either push folks to self-insure or turn to a private market insurance which she beleives goes against FEMA’s goals.

“You know there’s a lot of retired folks that, this will make a significant difference. If you’re looking at $500 a month increase, that’s a car payment, that is substantial," she said.

FEMA says, by law, most rate increases are capped at 18% per year. But in a report prepared to explain the flood insurance changes to clients and others, Holehouse illustrated how a $1,200 annual premium in 2021 could compound to $5,322 by 2030.

“I think that the long-term outlook is pretty scary when we start to look at these FEMA rates,” Holehouse said.

He believes the brunt of the impact will be felt by more than just homeowners with big waterfront “mansions.” He worries about what he describes as smaller, more “working class” homes that aren’t directly on the water but are still in flood-prone areas and require flood insurance.

Darcie Duncan, a realtor for Anna Maria Island and other coastal communities, fears there will be an impact.

“I personally feel that the market on the Island that the people who are going to be most affected are the people who are long-term residents,” she said. “Especially if you’re a retiree and you only have, you know, a fixed income, you tell me where you find the other $5,500 or $5,400 that you’re going to have to come up with.”

If you have flood insurance, Holehouse says it’s likely time to begin discussing the changes with your agent to determine how much you’ll be affected.

Congressman Charlie Crist blasted the changes and has called on House and Senate leaders to halt the program until it can provide full oversight and “implement appropriate affordability measures.”